What you need to know about UK IHT

What you need to know about UK IHT.

Passing assets efficiently to the next generation remains a primary objective for many who have spent a lifetime accumulating their wealth. By leaving a legacy, it is possible to provide funds for family members or a charitable interest in order to make life easier for others. Inheritance Tax is payable on everything you have of value when you die, including:

- your home,

- jewelry & watches,

- savings and investments,

- works of art, antiques

- cars,

- any other properties or land – even if they are overseas.

*pensions and life insurance policies are excluded.

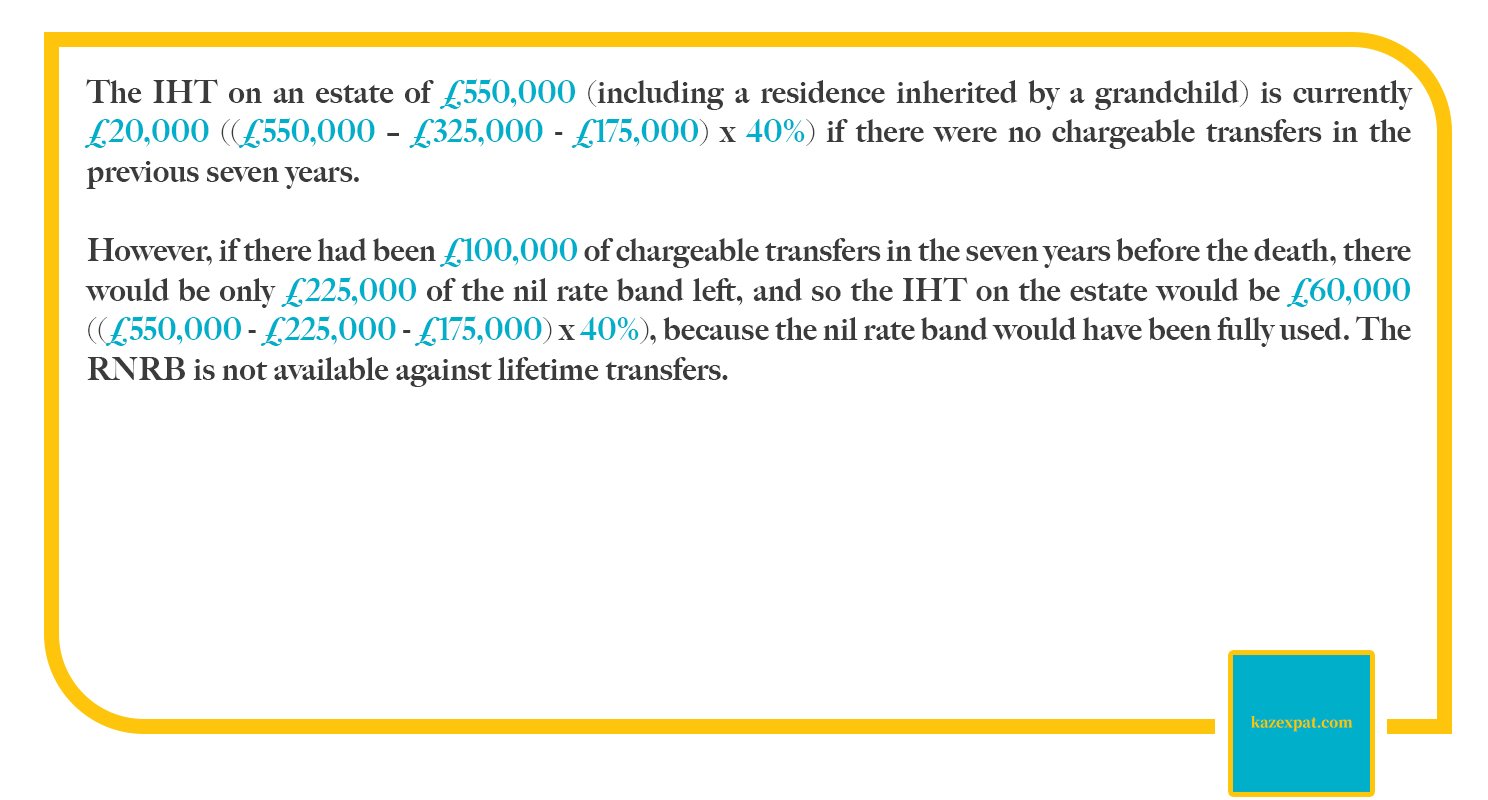

The current rate of inheritance tax for transfer values in excess of a nil rate band (NRB), currently £325,000 is 40%. Any part of your estate that is left to your spouse or registered civil partner will be exempt from Inheritance Tax. The exception is, if your spouse or registered civil partner is domiciled outside the UK. Then the absolute maximum you can give them before Inheritance Tax needs to be paid is £325,000. Where your estate is left to someone other than a spouse or registered civil partner, for example, to a non-exempt beneficiary, IHT will be payable on the amount that exceeds the nil rate band. If your spouse or civil partner dies before you, and did not use the whole of their nil rate band, the nil rate band applicable on second death can be increased by the percentage of nil rate band unused on the first death, provided your executors make the necessary elections within two years of your death.

Key information about UK inheritance tax.

With the average house price in the UK having increased 9.8% over the year to March 2022, you don’t have to be ‘wealthy’ to exceed the nil rate band. Therefore, the residence nil rate band (RNRB), introduced in 2017, allows a further £175,000 in addition to the normal £325,000 (NRB), and is intended to protect, at least partially, the family home (or in case of more than one home - the elected home) from IHT. The value of the home is after deducting any mortgage secured on the property. The RNRB is only available where a home is inherited on death by direct descendants, who may be the child (including a step-child, adopted child or foster child) of the deceased or their lineal descendants (i.e. grandchildren). The availability of the RNRB is protected where a person has downsized or ceased to own their own home after 7 July 2015 - provided assets of an equivalent value are then passed to direct descendants on death. For estates with a net value of more than £2 million, there is a reduction in the RNRB at a rate of £1 for every £2 over the £2 million. The RNRB is usually not available where a property is left to a discretionary trust.

Example 1:

Charge to IHT on lifetime transfers - what is an exempt transfer?

A lifetime transfer of value may be exempt, potentially exempt or immediately chargeable. It may also be taxable as a gift with reservation. In addition to the transfer of your estate on death to your surviving spouse or civil partner, HMRC permits you to give the following as exempt transfers:

- up to £3,000 each year as either one or a number of gifts. If you don’t use it all up one year, you can carry the remainder over to the next tax year.

- gifts of up to £250 to any number of other people – but not those who received all or part of the £3,000.

- any amount from income that is given on a regular basis provided it doesn’t reduce your standard of living. These are known as gifts made as ‘normal expenditure out of income’.

- if your child is getting married you can gift them £5,000, if a grandchild or more distant descendent is getting married £2,500, and a friend or anyone else you know £1,000.

- donations to charity, political parties, universities and certain other bodies recognised by HMRC.

- maintenance payments to spouses, and ex-spouses, elderly or infirm dependant relatives and children under 18 or in full-time education.

There are certain other gifts that can qualify for relief from Inheritance Tax. These can include gifts of a small business, sole trader enterprise or partnership and shares in companies listed on the smaller, more risky stock exchange, the Alternative Investment Market (AIM). Farmers can also gain up to 100% relief from Inheritance Tax when making gifts of certain agricultural land or farm buildings. But the rules in both these situations, known as Business Relief and Agricultural Relief respectively, are complex and you’d be best to seek expert advice before gifting anything away.

Members of the armed forces killed in action or whose death is hastened by injuries sustained on active duty are also exempt from Inheritance Tax.

Example 2:

Charge to IHT on lifetime transfers - what is a potentially exempt transfer (PET)?

You can also make larger gifts but these are known as Potentially Exempt Transfers (PETs) and you could have to pay Inheritance Tax on their value if you die within seven years of making them. A PET is a lifetime transfer by an individual to another individual, a bare trust or a disabled trust. No Inheritance Tax is charged at the date of the gift and HMRC does not have to be informed of the gift. If the donor then survives for seven years, the gift becomes an exempt transfer and will not be subject to Inheritance Tax.

However, if the doner dies within seven years, it is the individual (or Trust) which receives the gift which is liable to pay the Inheritance Tax and is based on the value of the gift on the date it was made, rather than the possibly lower/higher value at the date of death. The PET now becomes a chargeable transfer and Inheritance Tax is charged at 40% on the value exceeding the nil rate band of £325,000 subject to taper relief rates as a percentage reduction of between 20% - 80%.

Example 3:

Charge to IHT on lifetime transfers - what is a chargeable transfer?

Gifts made during your lifetime which do not qualify as exempt or a PET will immediately be chargeable to Inheritance Tax. These are called Chargeable Lifetime Transfers (CLT) and an example is a gift into a Discretionary trust.

All chargeable transfers over a seven-year period are added together and tax is immediately payable at 20% (i.e. half the rate of 40% which is charged on death) once the total exceeds the nil rate band of £325,000. The tax is based on the transferor’s cumulative total of transfers (other than exempt transfers), including the value transferred by any immediately chargeable lifetime transfer in the previous seven years, subject to any deductions for exemptions, reliefs, mortgages etc. A transfer drops out of the cumulation once it is more than seven years old. The tax is reduced by taper relief if the donor survives more than three years after the gift.

The taxation rules of CLTs are complicated and you should obtain professional advice if you are considering a CLT.

Charge to IHT on lifetime transfers - what is a gift with reservation?

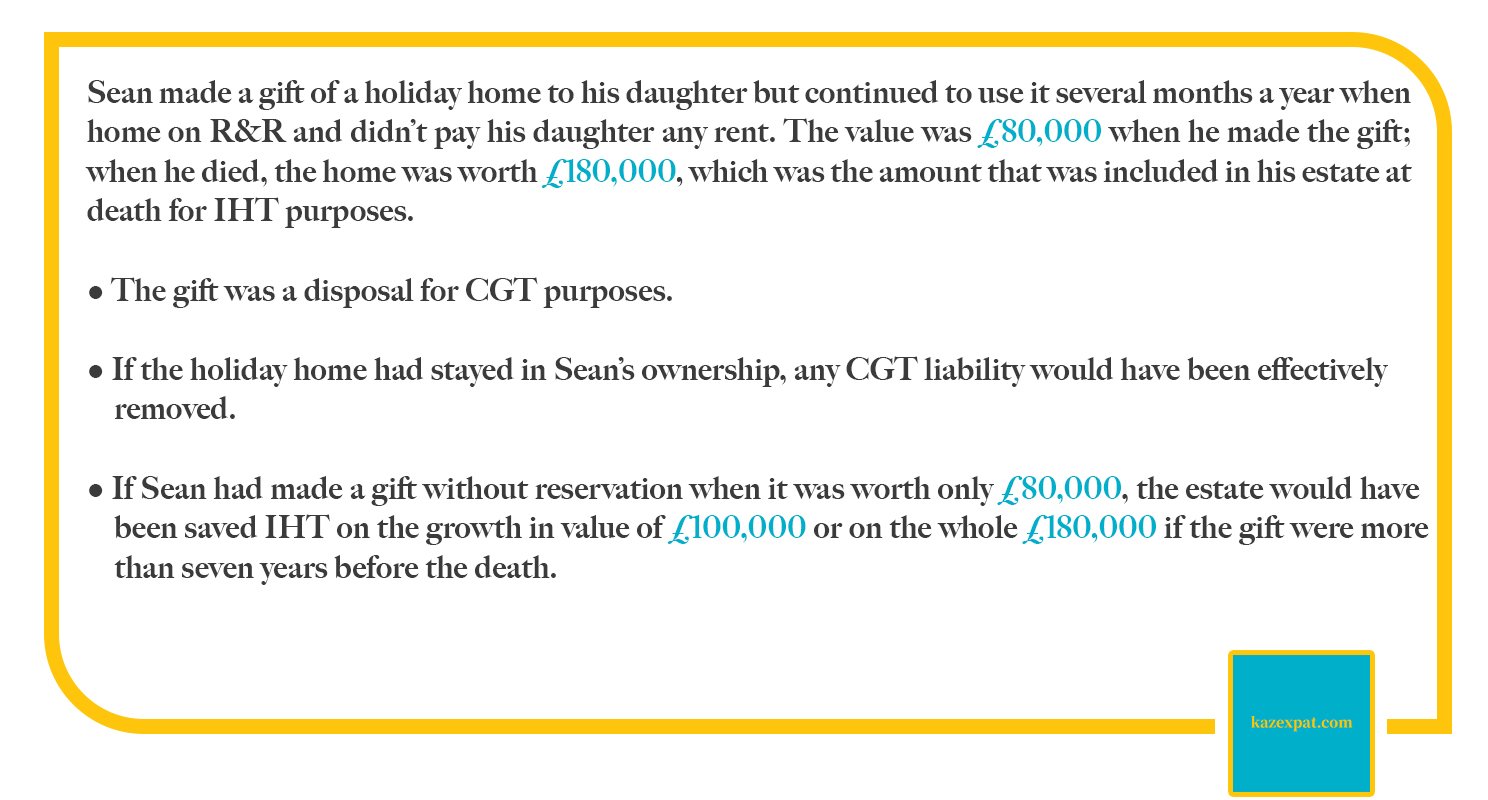

The most common example of a gift with reservation is if a parent gifts a house to their child but continues to live in the house rent-free. However, if later the parent pays a market rent, the gift becomes an outright gift and will be exempt if the parent survives another seven years. If the parent still retains a benefit in the gift at death, then the value of the gift becomes a chargeable transfer based on the value at the time of the gift. Another example of a gift with reservation is where the donor is a potential beneficiary under a discretionary trust where they continue to receive a benefit from the gift in trust. Therefore, standard advice would be for the donor to make sure they cannot themselves benefit in any way from the trust in order for the gift to be exempt from Inheritance Tax.

Example 4:

In conclusion, despite the introduction of the Resident Nil Rate Band offering an additional £175,000 threshold to protect, at least partially, the family home, Inheritance Tax bills will continue to grow in the coming years due to rising property values and a cap on the nil rate band of £325,000 until at least 2026.

That said there are many ways to manage, reduce, or eliminate an Inheritance Tax bill including making gifts, passing on your pension whilst using other assets to provide a retirement income, taking out life insurance to cover the tax bill, and using tax-efficient investments which offer relief.

Estate planning can save a huge amount of tax, and the savings can far outweigh the cost of advice. Taking action early means more of your money going to your beneficiaries and less to the taxman.

If you would like to discuss any area of personal finance, the author can be contacted at dermot.monaghan@holbornassets.com or simply use the Book A Call Back button at the bottom right of your screen.